What I Learned About Money When Sudden Illness Hit

It started with a fever and ended with a financial wake-up call. One moment I was living normally, the next I was facing medical bills, lost income, and zero emergency savings. That crisis taught me how fragile financial stability really is. I had always assumed that as long as I paid my bills on time and avoided debt, I was doing enough. But when illness struck without warning, I realized my sense of security was built on sand. The doctor visits, lab tests, and prescription costs added up quickly, and because I couldn’t work during recovery, my income vanished just when I needed it most. This experience exposed a truth many of us ignore: financial health isn’t just about earning or saving—it’s about resilience. If you’re starting from zero and worried about the unexpected, this is what I wish I’d known earlier—simple moves, real risks, and how to see the trends before they hit.

The Moment Everything Changed

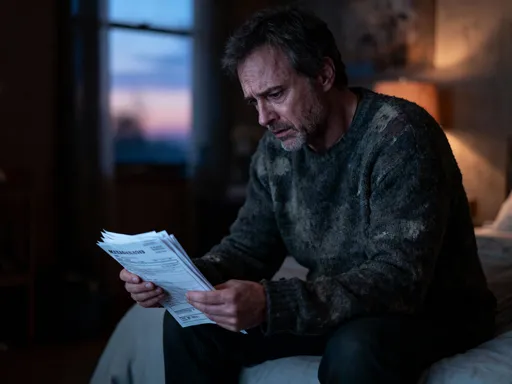

The first sign was a persistent fever that wouldn’t break. At first, I thought it was just a bad flu. I took over-the-counter medication, rested when I could, and tried to push through. But after three days of worsening symptoms, I went to the clinic. What followed was a series of tests, a diagnosis that required immediate treatment, and a hospital stay that lasted longer than expected. The medical bills began arriving before I even left the facility. Even with health insurance, the co-pays, deductibles, and out-of-network charges were staggering. I hadn’t anticipated that a single illness could generate thousands in expenses, not counting the medications and follow-up visits that would continue for months.

At the same time, my income stopped. I worked in a role that didn’t offer paid sick leave, and short-term disability wasn’t part of my benefits. My employer was understanding, but understanding didn’t pay the rent. I had to dip into my checking account, then start deferring non-essential bills. Within weeks, I was choosing between filling a prescription and keeping the lights on. The emotional toll was just as heavy as the financial one. I felt isolated, ashamed, and overwhelmed. I had always considered myself responsible—budgeting, avoiding credit card debt, living within my means. But none of that mattered when the system I depended on collapsed under pressure. That’s when I realized: feeling financially secure isn’t the same as being secure. True stability isn’t measured by how much you earn or spend, but by how well you can withstand a shock.

What made the situation worse was the lack of preparation. I didn’t have an emergency fund. I had never seriously considered what would happen if I couldn’t work for more than a week or two. Like many people, I assumed emergencies were things like car repairs or home leaks—disruptive, but manageable. A sudden health crisis that removed both my health and income simultaneously was beyond my mental model of risk. The gap between my assumptions and reality was enormous. I had built my financial life on continuity, but life doesn’t guarantee continuity. That moment of crisis became a turning point—not just in my health, but in how I understood money. It wasn’t about budgeting anymore. It was about survival, foresight, and the quiet power of being ready.

Why Most Beginners Ignore Emergency Risk (And Pay Later)

One of the most common financial blind spots is the belief that emergencies won’t happen to us. This mindset isn’t rare—it’s nearly universal among people who haven’t yet faced a major disruption. The phrase “It won’t happen to me” is more than just optimism; it’s a psychological defense mechanism. We tell ourselves we’re careful, healthy, or lucky enough to avoid serious problems. We assume that insurance will cover everything, that our job is stable, or that we’ll have time to react if something goes wrong. These beliefs create a false sense of security, one that often holds until it doesn’t. When the unexpected finally arrives, the cost isn’t just financial—it’s the price of being unprepared.

Another major misconception is overestimating the protection offered by health insurance. Many people assume that having coverage means they’re shielded from high costs. But in reality, insurance rarely covers 100% of medical expenses. High deductibles, co-insurance, prescription costs, and non-covered treatments can leave patients responsible for thousands of dollars—even for routine care. And if the illness requires time off work, there’s no insurance for lost income unless you’ve specifically purchased disability coverage, which most people haven’t. The gap between what insurance pays and what you owe can be wide, and without savings to bridge it, families are forced into difficult choices: depleting retirement accounts, borrowing from family, or taking on high-interest debt.

There’s also a tendency to delay financial preparation because it feels overwhelming. When you’re already managing daily expenses, adding another financial goal—like building an emergency fund—can seem impossible. The idea of saving several months’ worth of living expenses feels like a mountain, especially if you’re living paycheck to paycheck. So instead of starting small, many people do nothing. They tell themselves they’ll begin “next month” or “when things settle down.” But life rarely settles down. Emergencies don’t wait for perfect timing. The irony is that the people most vulnerable to financial shocks are often the ones least likely to prepare, not because they don’t care, but because they feel powerless to act. Overcoming this inertia requires a shift in mindset: preparation isn’t about perfection. It’s about progress, one small step at a time.

The Hidden Cost of Waiting: How One Crisis Exposes Your Financial Weak Spots

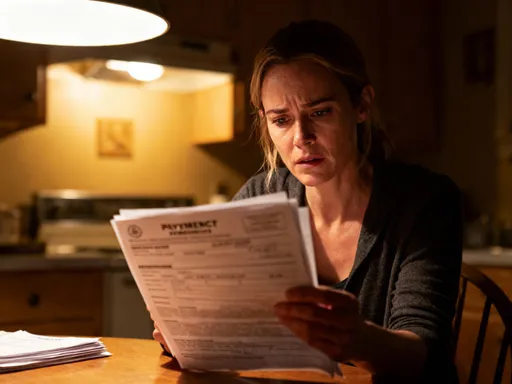

When a sudden illness hits, the immediate costs are only part of the story. The real damage often comes from the ripple effects—the indirect consequences that compound over time. Lost wages are one of the most significant but overlooked impacts. Even a two-week absence from work can mean missing hundreds or thousands of dollars in income, depending on your job. For hourly workers or freelancers, the loss is immediate and total. Unlike salaried employees who might have some paid time off, many people have no safety net when they can’t work. This income gap forces difficult decisions: using credit cards to cover basics, delaying bill payments, or asking for help from family. Each of these choices carries long-term consequences.

Using credit to cover emergency expenses can lead to a cycle of debt that’s hard to escape. High-interest rates mean that a $3,000 medical bill paid on a credit card could end up costing $4,000 or more over time. Missed payments damage credit scores, which in turn affect the ability to rent an apartment, buy a car, or secure future loans. A single crisis can trigger a downward spiral that lasts years. Even if the illness itself is temporary, the financial damage can be permanent. And for families, the strain doesn’t stop with the individual. Partners may have to take on extra shifts, children might feel the stress at home, and relationships can become strained under the weight of financial pressure.

Another hidden cost is the loss of momentum in long-term financial goals. When you’re in crisis mode, retirement savings, college funds, or home-buying plans are often put on hold. What feels like a temporary pause can become a permanent setback. Studies show that people who experience a major financial shock are less likely to resume saving at the same rate, if at all. The psychological impact of falling behind can lead to disengagement from financial planning altogether. This is why waiting to prepare is so dangerous—it doesn’t just leave you vulnerable to the next crisis. It weakens your ability to recover from the last one. Financial resilience isn’t just about avoiding disaster. It’s about maintaining stability so that one setback doesn’t derail your entire future.

Building Your First Financial Safety Net: No Jargon, Just Steps That Work

The good news is that building financial resilience doesn’t require a high income or complex strategies. It starts with small, consistent actions that add up over time. The foundation of any safety net is an emergency fund—a dedicated pool of money set aside for unexpected expenses. The goal isn’t to save six months of expenses overnight. It’s to start with what you can. Even $500 can make a difference in covering a car repair or a medical co-pay without resorting to debt. The key is to make saving automatic and non-negotiable, just like paying a bill. Setting up a direct deposit from your paycheck into a separate savings account removes the temptation to spend that money elsewhere.

Choosing the right account matters. Your emergency fund should be kept in a safe, liquid account—meaning you can access it quickly when needed. A high-yield savings account is ideal because it earns more interest than a regular savings account while still allowing easy access. Unlike investments, which can lose value, cash in a savings account is stable and protected by federal insurance up to certain limits. Avoid putting emergency funds into retirement accounts, stocks, or long-term CDs, where withdrawal penalties or market fluctuations could make the money unavailable when you need it most.

Tracking expenses is another essential step. You don’t need a complicated budget—just a clear picture of where your money goes each month. This awareness helps identify areas where you can redirect small amounts toward savings. Maybe it’s packing lunch instead of buying it, switching to a cheaper phone plan, or pausing a subscription service. These changes don’t require drastic lifestyle shifts, but they create space in your budget for building security. The goal isn’t deprivation. It’s intentionality. Every dollar saved is a brick in your financial foundation. Over time, those bricks form a wall strong enough to withstand life’s surprises.

Reading the Signals: How to Spot Financial Trends Before They Hit You

Financial preparedness isn’t just about reacting to crises—it’s about anticipating them. Just as weather patterns can be studied to predict storms, personal and societal trends can offer early warnings about potential risks. One of the most important signals is the rising cost of healthcare. Even if you’re healthy now, medical expenses have been increasing faster than inflation for decades. Prescription drugs, specialist visits, and routine screenings are all becoming more expensive. If your insurance premiums or deductibles have gone up recently, that’s not just a one-time change. It’s part of a larger trend that will likely continue. Recognizing this allows you to plan ahead rather than be blindsided.

Another signal is job stability and income flexibility. Are you dependent on a single source of income? Does your job offer paid leave or remote options if you get sick? The shift toward gig work and contract positions has given people more freedom, but it has also reduced financial security for many. Without employer-sponsored benefits, individuals must take on more responsibility for their own safety net. If your work doesn’t provide disability coverage or paid sick days, that’s a gap you need to address proactively. Similarly, if your industry is undergoing changes—automation, downsizing, or market shifts—it’s wise to build extra cushioning in case of income disruption.

Personal habits also send signals. Do you frequently use credit cards to cover monthly expenses? Are you consistently living up to your income limit? These behaviors indicate low financial margin, which means even a small setback could become a crisis. By monitoring your own patterns—how much you save, how often you dip into reserves, how easily you handle small emergencies—you gain insight into your true level of preparedness. Awareness isn’t about fear. It’s about empowerment. When you see trends early, you can adjust gradually, avoiding the need for drastic measures later. Preparation becomes a habit, not a panic response.

Balancing Risk and Reward: Smart Moves That Won’t Break the Bank

In times of uncertainty, the instinct to chase high returns can be strong. After a financial setback, there’s often a desire to “make up” for lost ground quickly. This can lead to risky decisions—investing in volatile stocks, trying speculative side hustles, or borrowing money to start a business. While these strategies have their place for some, they are not the foundation of recovery. For most people, especially those rebuilding after a crisis, the priority should be capital preservation, not capital growth. Protecting what you have is more important than trying to gain more.

An emergency fund is the ultimate low-risk, high-reward tool. It doesn’t offer market returns, but it provides stability, peace of mind, and the ability to avoid high-cost debt. The return on an emergency fund isn’t measured in interest—it’s measured in avoided fees, saved credit scores, and reduced stress. When you have a buffer, you’re less likely to make emotional financial decisions under pressure. You can take time to evaluate options, negotiate medical bills, or wait for a better job opportunity instead of accepting the first offer out of desperation.

Low-risk financial habits create long-term advantages. Automating savings, paying down high-interest debt, and maintaining insurance coverage aren’t flashy strategies, but they build resilience over time. They reflect discipline rather than luck. The difference between those who survive financial shocks and those who don’t often comes down to these quiet, consistent choices. It’s not about earning more. It’s about managing what you have with intention. In the face of uncertainty, stability is the greatest reward.

Turning Crisis Into Control: A Realistic Path Forward

Looking back, I wouldn’t wish that illness on anyone. But I also wouldn’t undo the lessons it taught me. Financial confidence isn’t about having a lot of money. It’s about knowing you can handle what comes your way. That confidence doesn’t come from luck or privilege. It comes from preparation—small, consistent actions that build resilience over time. The most powerful financial tool isn’t a stock tip or a side hustle. It’s awareness. The ability to see risks before they hit, to act before you’re forced, and to make choices from a place of strength rather than fear.

You don’t need to be perfect. You don’t need to save thousands overnight. You just need to start. Open a separate savings account. Set up a $25 automatic transfer. Track your spending for one week. These steps may seem small, but they are the beginning of control. They shift your relationship with money from reactive to proactive. And when the next challenge comes—because it will—you’ll be ready. Not because everything is solved, but because you’ve built the habit of solving it. Financial readiness isn’t a destination. It’s a practice. And like any practice, it grows stronger with time. Start now, start small, and let that small beginning become the foundation of lasting security.